Uber's $10 billion illusion

How deferred tax releases and unrealized gains hijacked two years of earnings headlines — and why the real story is actually better than the reported one.

Uber reported $9.9 billion in net income in 2024. Then $10.1 billion in 2025. Headlines celebrated the numbers. Analysts updated their models. Investors felt confirmed. There was just one problem: the company that generated those profits barely exists.

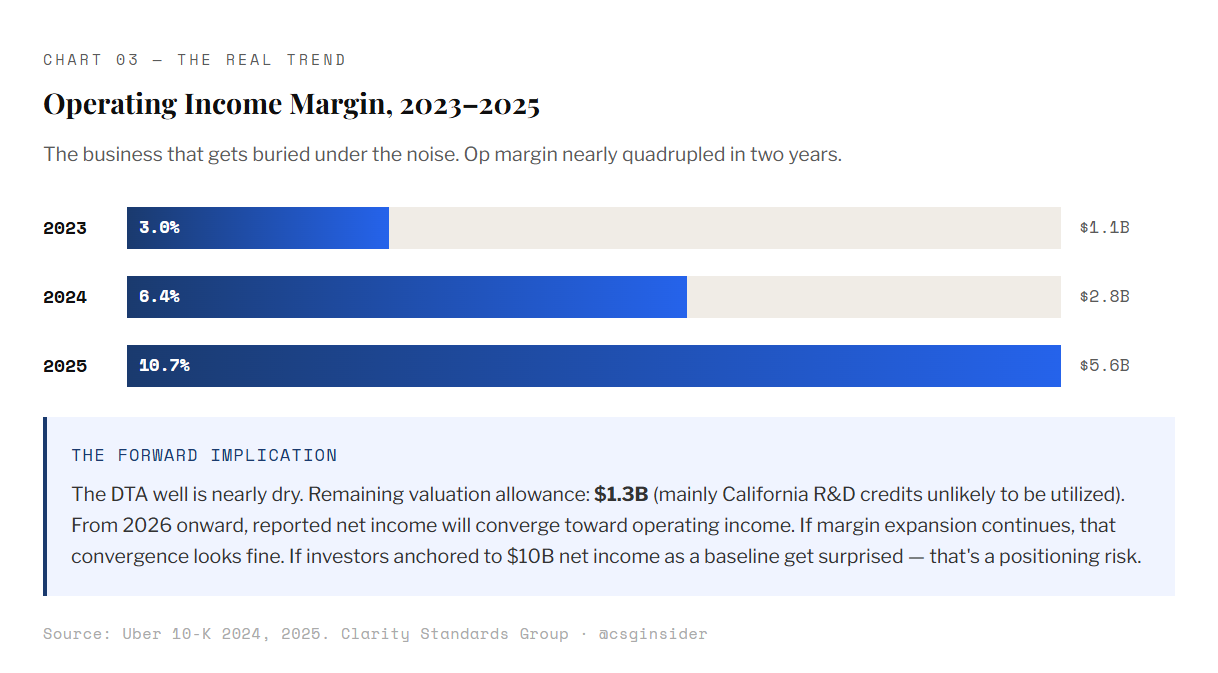

The real Uber — the one that picks up riders, delivers burritos, and hauls freight — earned $2.8 billion in 2024 and $5.6 billion in 2025. Not bad numbers. Actually excellent numbers when you understand the trajectory. But they’re not the numbers most people are watching.

Beneath the headline figures sits a layer of non-operating noise so large it has effectively decoupled reported net income from actual business performance for two consecutive years. Understanding that noise is the difference between investing in a story and investing in a company.

The Tax Shelter That Wasn’t a Tax Shelter

For most of its life as a public company, Uber carried an enormous pile of deferred tax assets — NOL carryforwards, stock compensation deductions, research credits — that it couldn’t recognize because it wasn’t profitable enough to use them. The accounting treatment is straightforward: you set up a valuation allowance against deferred tax assets you believe are unlikely to be realized. Uber’s valuation allowance peaked at nearly $14 billion.

When a company finally turns the corner on sustained profitability, that allowance gets released. The release flows through the income statement as a tax benefit — a one-time, non-cash, non-recurring gain that has nothing to do with current year operations. The more profitable you become, the bigger the release.

In 2024, Uber released $7.9 billion of its US federal and state valuation allowance. The income statement booked a $6.4 billion tax benefit. In 2025, the Netherlands subsidiary followed suit — $5.0 billion released, $5.0 billion tax benefit recognized. Combined over two years: $11.4 billion of non-cash tax benefit injected into reported net income.

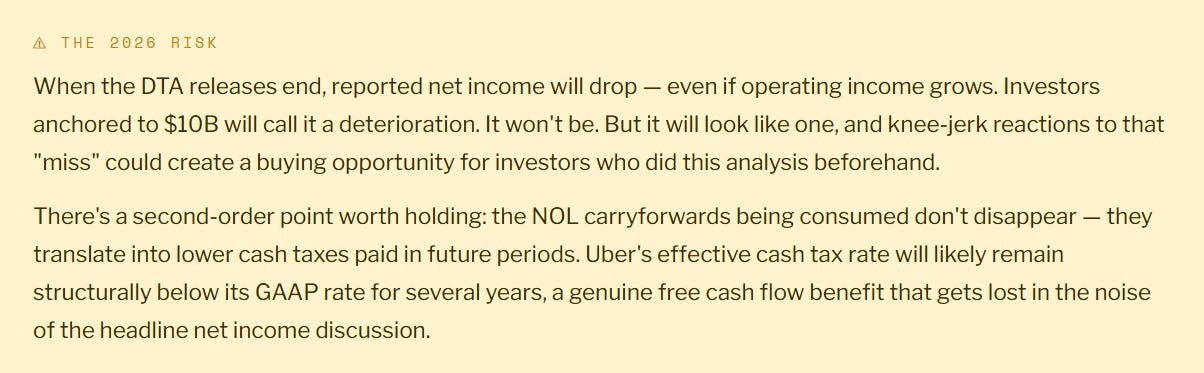

To be clear: this accounting is correct, and the underlying signal is genuinely good news. PwC signed off. The more-likely-than-not threshold under ASC 740 is legitimately satisfied when a company demonstrates sustained profitability — and Uber earned it. The $11B DTA balance now sitting on the balance sheet represents real future value: as those NOL carryforwards are consumed in coming years, Uber will pay less cash tax than its GAAP provision implies, a structural tailwind for free cash flow that extends several years forward.

The analytical problem isn’t the release itself — it’s the income statement pop it creates. That one-time catch-up entry is a backward-looking accounting recognition of a business improvement that already happened. It is not a forward earnings signal. And investors who anchor to the $9.9B or $10.1B headline as a baseline for future expectations are conflating the two.

“The DTA release is justified and genuinely positive. But, the income statement pop is a backward-looking catch-up entry, not a forward earnings signal. Those are two different things.”

— Clarity Standards Group

The Investment Portfolio That Moves Your EPS

Layered on top of the DTA noise is a second source of income statement volatility: Uber’s portfolio of minority equity stakes in companies like Aurora (autonomous vehicles), Grab (Southeast Asia ride-share), and Didi (China). These are marked to market through the income statement each quarter — not through other comprehensive income, which is where most companies park unrealized investment gains and losses.

In 2024, this portfolio contributed a $1.8 billion gain to pre-tax income. Aurora’s stock ran, Didi recovered, Grab rallied. In 2025, the same portfolio swung to a net $97 million loss — Aurora gave back most of its gains, Lucid (a newer position) declined. Uber’s operating business earned significantly more in 2025 than 2024. Its investment portfolio performance was essentially irrelevant to that fact. Yet both figures flowed through the same income statement line.

The result is an income statement where a $629 million unrealized gain on Aurora’s stock price has the same accounting weight as $629 million of earned service fees. Most readers don’t distinguish between them. The footnotes do.

Uber’s Number vs. GAAP’s Number

To be fair to Uber, the company knows its GAAP net income is noisy. That’s why management leads every earnings call with Adjusted EBITDA — $6.5 billion in 2024, $8.7 billion in 2025. It’s the number in the press release headline, the number in the investor presentation, the number the sell-side models on.

Adjusted EBITDA is useful. It adds back depreciation and amortization (real but non-cash), stock-based compensation (real and very much cash-equivalent in economic terms, but that debate is for another day), and strips out the noise below the operating line. For a capital-light marketplace business, it does capture something real about cash generation.

But it also excludes things worth knowing about. Stock-based compensation of $1.8 billion annually is not a fiction — Uber is diluting shareholders to compensate employees, and that cost is real. More importantly, Adjusted EBITDA doesn’t tell you about the operating leverage story because it obscures D&A trends and lumps in SBC add-backs of varying economic significance.

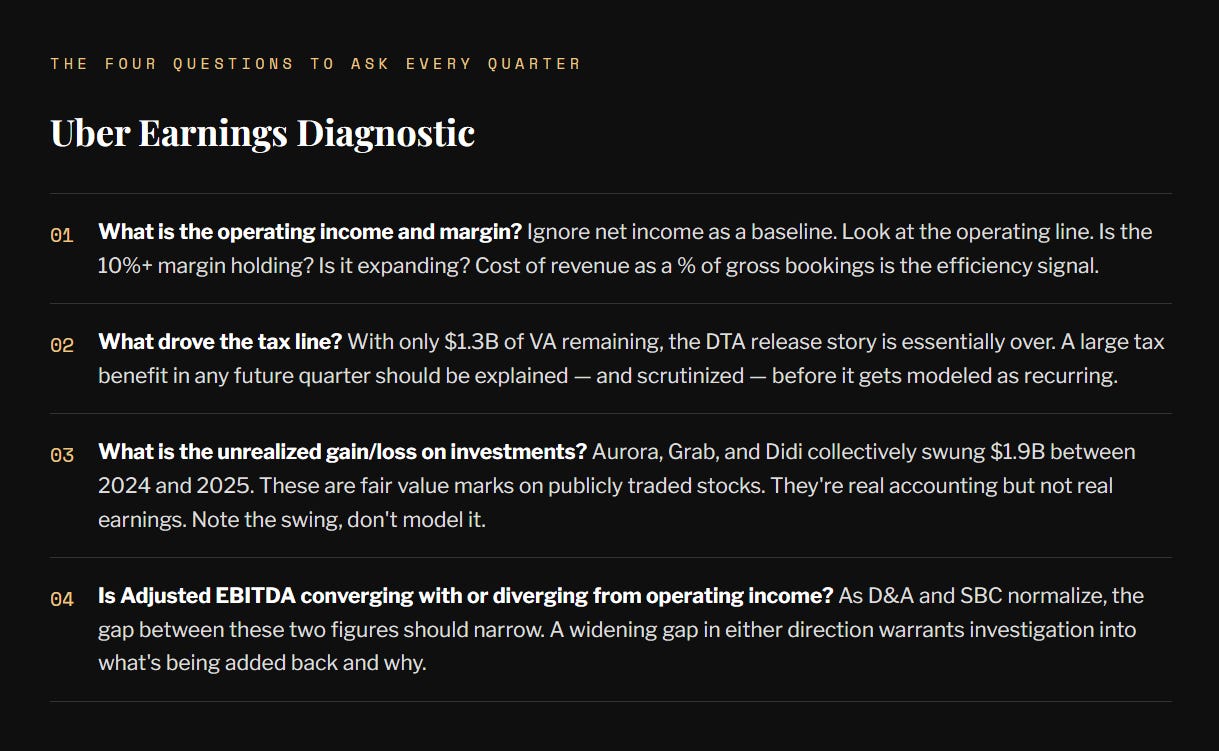

Our preferred lens: operating income. It’s fully GAAP, it’s below the revenue line so it captures cost discipline, it’s above the interest and investment noise, and it strips out the DTA releases automatically. The trajectory in that number is the most honest thing in Uber’s financials: $1.1B → $2.8B → $5.6B across three years. That’s the story.

“Adjusted EBITDA adds back real costs. GAAP net income adds in accounting fictions. Operating income sits between them and tells the truth.”

— Clarity Standards Group

What the Auditors Said — and What They Didn’t

PwC’s Critical Audit Matters in both filings tell you exactly where the judgment calls live. Two items appear in both years: the principal vs. agent determination for Mobility and Delivery revenue, and the valuation of insurance reserves. The DTA release does not appear as a CAM in either year — meaning the auditors were satisfied that Uber’s more-likely-than-not assessment was well-supported and did not require elevated scrutiny. That’s actually good news for the revenue recognition picture.

What PwC is telling you with the insurance reserve CAM, however, is less comfortable: $12.5 billion in total insurance reserves as of year-end 2025, growing at $4.9 billion per year in additions against only $2.4 billion in annual claims paid. The reserve-to-claims ratio is 5.1x. The long tail on auto liability claims means this is probably appropriate, but it also means Uber is sitting on a liability that is 140% of its annual operating income. That’s a separate article. Stay tuned.

The bigger takeaway from the audit opinion: Uber’s revenue recognition is getting cleaner over time, not messier. The business model changes from 2023 that reclassified promotions as contra-revenue in certain markets were a one-time complexity, not a recurring one. The auditors flagged it in 2024 as a CAM. In 2025, the same item remains, but the dollar magnitude of affected transactions is known and bounded.

Bottom Line

Uber’s net income over the past two years is a masterclass in why reading the income statement top-to-bottom matters more than reading the headline.

The company released $11.4 billion in non-cash deferred tax benefits across 2024 and 2025, inflating reported net income to levels that bear no resemblance to operating cash generation. Add in $1.7 billion of net unrealized investment gains in 2024 and the picture is thoroughly distorted.

The operating story is actually excellent. A business that went from 3% to 10.7% operating margins in two years, with gross bookings growing 19% and free cash flow of $9.8 billion in 2025, is a strong business. But that story gets buried every time a reporter leads with “$10 billion profit.”

The DTA well is nearly dry. From 2026 onward, reported earnings will look very different — closer to operating income, less inflated. The NOL carryforwards being consumed don’t vanish; they translate into lower cash taxes paid over several years, a genuine free cash flow tailwind. But that subtlety won’t make it into the headline. Investors who understand the mechanics won’t be surprised. Everyone else will call it a deterioration.

The footnotes knew. Almost nobody read them. — Clarity Standards Group